How Real-Time Analytics Transform Insurance Pricing and Concentration Risk Detection

Insurance | May 7, 2026

Perceptive Analytics’ Perspective — Why This Matters Now

Insurance pricing has always been probabilistic. What has changed is the time available to respond. Annual or quarterly pricing cycles made commercial sense when the dominant risk signals were actuarial triangles, demographic proxies, and historical loss development. They do not make sense in a market where climate events concentrate losses in weeks, social inflation shifts liability costs quarter-to-quarter, and telematics feeds update individual risk profiles continuously.

At Perceptive Analytics, we work with pricing and risk leaders who are under simultaneous pressure to improve pricing adequacy, reduce adverse selection, and contain concentration risk — without destabilising the underwriting portfolio in the process. Real-time analytics is not a solution to all of these pressures. But it is the capability gap that makes the other pressures harder to manage than they need to be.

This guide maps the data sources, tools, integration patterns, and business case for real-time analytics in pricing and risk — grounded in current industry practice, not aspirational technology marketing.

The market context for real-time pricing and risk analytics has sharpened considerably in 2024 and 2025. Insured natural catastrophe losses reached $140 billion globally in 2024 — the third-highest level on record — led by Hurricanes Helene and Milton [Munich Re, 2024]. Social inflation continues to drive liability claims severity, with liability costs rising 57% over the past decade driven by nuclear verdicts and expanding litigation funding [n2uitive / Industry Research, 2025]. And according to Verisk’s 2025 Annual Insurance Claims Trends Report, even as overall claims volume declined in 2025, the underlying loss patterns told a different story: risk became more complex, more concentrated, and harder to detect through conventional monitoring [Verisk, 2025].

Against this backdrop, 83% of insurance executives believe predictive models are critical for underwriting’s future [Capgemini, World P&C Insurance Report, 2024]. But belief is not implementation: only 29% of insurance companies globally use AI-driven models that could support real-time pricing decisions [Goldman Sachs Global Insurance Survey, 2024]. The gap between aspiration and execution is where competitive advantage is being built — and lost.

Munich Re, 2024

n2uitive, 2025

Want to understand which real-time pricing use case delivers the highest ROI for your portfolio?

Talk with our consultants today.

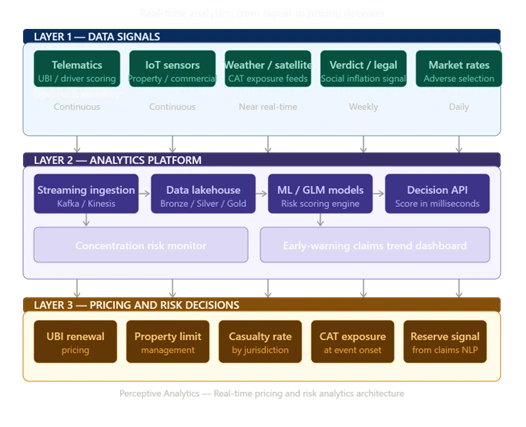

1. Real-Time Data Sources Insurers Are Feeding into Pricing Models

Modern insurance pricing is moving from static, demographic-based segmentation toward dynamic, signal-driven models. The shift is structural: when risk profiles change continuously — due to driving behaviour, weather exposure, property condition, or litigation trends — pricing models that update annually are always lagging the portfolio they are supposed to describe.

Telematics and Behavioural Driving Data

In 2024, more than 21 million US policyholders shared telematics data with their insurer — a 28% compound annual growth rate since 2018 [IoT Insurance Observatory / Carrier Management, 2026]. The global insurance telematics market, valued at $6.8 billion in 2024, is projected to grow at 18.9% CAGR through 2034 [GM Insights, 2025]. The signals captured — acceleration, braking force, cornering, time of day, route selection, mileage — replace demographic proxies with observed individual behaviour, enabling segmentation that legacy rating factors simply cannot replicate.

IoT Sensors: Property and Commercial Risk

Beyond auto, IoT devices in homes and commercial properties generate continuous signals on occupancy, water flow, structural stress, and fire risk. The broader IoT insurance market was valued at $48.3 billion in 2024 and is projected to reach $483.2 billion by 2033 at a 29.2% CAGR [IMARC Group, 2024]. For property underwriters, smart sensor data shifts pricing from a point-in-time exposure assessment to a continuously updated risk profile.

Weather, Climate, and Geospatial Feeds

Real-time meteorological feeds from providers including The Weather Company and Tomorrow.io, combined with satellite imagery and geospatial data, enable insurers to update catastrophe exposure calculations as events develop. In 2024, a leading analytics firm launched a geospatial platform using 4K satellite imagery to monitor 100% of high-risk flood zones — improving risk prediction accuracy by 28% for property insurers [Mordor Intelligence, 2026].

External Financial and Legal Signals

Social inflation — the upward pressure on claims costs driven by litigation funding, nuclear verdicts, and expanding attorney representation — is not visible in historical loss triangles until the damage is done. Leading carriers are integrating legal data feeds: verdict databases, litigation filing rates by jurisdiction, and third-party litigation funder activity, as forward-looking signals for casualty and liability pricing adjustments.

Market and Competitive Pricing Signals

Real-time competitive rate monitoring — tracking where market prices are moving by segment and geography — enables pricing teams to identify adverse selection risk before it manifests in the loss ratio. When the market softens in a segment where your pricing has not moved, you are systematically attracting the risks the competition is avoiding.

| Data Source | Signal Type | Primary Pricing Application | Update Frequency |

|---|---|---|---|

| Telematics / mobile apps | Behavioural | UBI pricing, driver risk scoring | Continuous |

| IoT sensors (home/commercial) | Structural/environmental | Property pricing, loss prevention | Continuous to daily |

| Weather / satellite feeds | Environmental | Catastrophe exposure, peril pricing | Near real-time |

| Verdict / litigation databases | Legal/social | Casualty pricing, social inflation adjustment | Weekly to monthly |

| Competitive rate feeds | Market | Adverse selection detection, rate positioning | Daily to weekly |

| Credit and financial data | Economic | Commercial risk scoring, renewal pricing | Monthly |

2. Impact of Real-Time Signals on Pricing Accuracy and Efficiency

The business case for real-time pricing signals is grounded in measurable improvements across three dimensions: pricing adequacy, adverse selection reduction, and portfolio stability. The evidence base has strengthened considerably in the past two years.

- Pricing accuracy: P&C insurers implementing predictive modelling in underwriting experienced a 67% improvement in risk assessment accuracy and a 5.7% decrease in combined ratios, according to a 2024 Willis Towers Watson study. Premium leakage — the gap between charged and technically adequate premium — fell by approximately $14 million per $1 billion of written premium [WTW, 2024].

- Loss ratio improvement: 74% of insurers have successfully reduced their loss ratios by at least 3% to 5% through the implementation of real-time risk assessment tools [Mordor Intelligence, 2026]. Allstate’s telematics programme achieved a 27% improvement in loss ratios through granular risk segmentation across its personal auto book [Softwebsolutions, 2025].

- Adverse selection reduction: Real-time pricing signals enable dynamic segmentation that makes it significantly harder for high-risk insureds to be mispriced into the portfolio. Machine learning models that integrate telematics data can predict accident likelihood before incidents occur, allowing targeted pricing adjustments rather than portfolio-wide rate corrections.

- Pricing cycle compression: Where traditional pricing reviews run quarterly or annually, real-time signal integration allows pricing teams to monitor adequacy and trigger model updates on a rolling basis — compressing the lag between risk change and price response from months to weeks.

WTW, 2024

WTW, 2024

The efficiency gains compound the accuracy improvements. AI-driven underwriting automation has reduced policy processing times by 50–70% and decreased administrative costs by 30% at carriers that have implemented it [Accenture Insurance Technology Vision, 2024]. These gains free actuarial and pricing capacity from routine processing to model development, validation, and interpretation — the work that requires domain expertise.

3. Core Platforms and Tools for Integrating Real-Time Signals

The technology stack for real-time insurance pricing analytics is not a single platform — it is a deliberately assembled set of components, each playing a defined role in the data flow from signal capture to pricing action.

Cloud Data Lakehouse Platforms

Cloud-native lakehouse environments — Snowflake, Databricks, Google BigQuery, Azure Synapse — are the foundational layer. They provide the scalable storage and compute needed to ingest and query heterogeneous data at volume: structured policy records alongside unstructured sensor streams and geospatial imagery. Cloud spending in insurance is projected to grow from 59% of the total addressable market in 2025 to 72% by 2029 [Gartner, July 2025], reflecting the consensus that cloud-native architecture is the prerequisite for analytics at the speed and scale modern pricing requires. See our Snowflake data transfer case study for a real-world example of this pattern in a high-volume, multi-country data environment.

Streaming and Event-Driven Ingestion

Streaming platforms — Apache Kafka, AWS Kinesis, Azure Event Hubs — enable real-time data ingestion from telematics devices, IoT sensors, and weather feeds. They replace batch overnight loads with continuous data flows, ensuring the pricing environment is current throughout the business day rather than updated once at end-of-day. Without streaming infrastructure, the ‘real-time’ in real-time pricing is a marketing claim rather than an operational reality. Talend consulting capabilities are particularly relevant for designing and maintaining these streaming ETL pipelines at the data quality and governance standards insurance pricing requires.

Actuarial and Machine Learning Modelling Environments

Generalised linear models (GLMs) remain the actuarial backbone for rate filings and explainability requirements. Machine learning models — gradient boosting, neural networks, random forests — augment GLMs with the ability to capture non-linear interactions in high-dimensional data. The most effective pricing environments use both: GLMs for the regulatory filing and rate schedule, ML models for the risk scoring layer that feeds into rating variables.

Real-Time Risk Scoring and Decision APIs

Translating model outputs into pricing decisions at point-of-quote requires an API layer that returns a risk score — and, in fully integrated environments, a premium recommendation — in milliseconds. This is the bridge between the modelling environment and the underwriting workbench or agent portal. Carriers that have built this bridge report significantly faster quote issuance on complex risks as well as more consistent pricing across the portfolio.

BI and Risk Dashboards

Tableau and Power BI, deployed against the governed data environment, provide the self-service analytics layer through which pricing analysts and actuaries monitor model performance, segment loss ratios, and identify emerging trends without requiring data engineering support. The most effective risk dashboards include real-time KPI feeds — loss ratio by segment and quarter, hit ratio trends, claim frequency heat maps — that surface early warnings before they appear in actuarial triangles. See Perceptive Analytics’ workforce efficiency utilization dashboard and pipeline analysis dashboard as examples of how this self-service analytics layer works in practice.

4. Analytics Approaches for Concentration Risk and Emerging Claim Trends

Concentration risk — the accumulation of correlated exposures that can produce correlated losses in a single event — is one of the most persistent and least visible threats to insurance portfolio stability. The 2025 Los Angeles wildfires, which produced $35–$40 billion in insured losses and disproportionately impacted densely populated communities with higher home values, demonstrated how quickly concentration risk can translate into capital events for primary insurers [IRMI, 2025].

Perceptive’s POV — The Concentration Problem

Concentration risk is invisible until it is not. A carrier can write a geographically diversified book on paper — spread across 30 states, 15 lines of business — and still be acutely concentrated in social inflation exposure if casualty lines are heavy in the jurisdictions with the highest nuclear verdict rates. Or concentrated in secondary peril exposure if property limits are high in flood zones that do not appear in the PML model.

At Perceptive Analytics, we find that concentration risk analytics delivers its highest value not in detecting large, obvious accumulations — those are usually managed — but in surfacing the subtle correlations that are invisible in traditional portfolio views: the same general contractor appearing in 40 commercial property risks, the same attorney firm appearing in 120 bodily injury claims, the same ZIP code cluster generating 18% of a coastal book’s expected losses.

Geospatial Accumulation Analytics

Geocoded policy data, combined with high-resolution peril models, enables carriers to calculate exposure concentration at the parcel level — not just by ZIP code or county. When overlaid with real-time catastrophe event footprints, this capability answers the question that historically could only be answered after a catastrophe event: ‘What is our exposure in this event footprint, by limit, by line, by deductible structure?’ Climate-related insured losses hit $137 billion in 2024, prompting carriers to model peril exposure at exactly this resolution [Mordor Intelligence, 2026].

Early-Warning Claim Trend Detection

Claims data is often the earliest signal of how risk is changing — before it appears in pricing adequacy metrics or reserve development. As Verisk’s 2025 Annual Claims Trends Report observed, emerging trends such as PFAS-related claims and silica dust claims rose from minimal volumes to hundreds or thousands of claims within 12–18 months, signalling emerging loss exposures that warrant proactive pricing and underwriting responses [Verisk, 2025]. The analytics approach for trend detection involves monitoring claim narrative text through NLP, tracking emerging cause-of-loss codes, and flagging statistical anomalies in claim frequency or severity at a segment level before they reach actuarial materiality. For a real-world data extraction example, see our automated data extraction case study.

Social Inflation Monitoring by Jurisdiction

Nuclear verdict databases and litigation filing rate analytics by jurisdiction enable casualty underwriters to identify where social inflation is accelerating — and to build forward-looking pricing adjustments rather than responding to loss development that has already occurred. Rising liability loss trends, driven by a record number of social inflation-fuelled nuclear verdicts, have created a complex casualty pricing environment in the US, with similar concerns emerging in the UK and Europe [Aon, 2025].

Counterparty and Third-Party Concentration Analytics

Commercial lines concentration risk is not only geographic. High concentrations in specific industries, supply chains, or counterparties — the same named insured appearing across multiple policy types, or the same service provider appearing in a disproportionate share of claims — create correlated exposure that standard accumulation tools miss. Graph analytics and network analysis are emerging as the appropriate technique for detecting these non-geographic concentrations.

5. Integrating Early-Warning Analytics with Existing Systems and Workflows

The integration question is where most analytics initiatives fail. A model that produces an accurate risk score but is not connected to the underwriting workbench, the pricing engine, or the catastrophe monitoring workflow is an analytics capability that exists in isolation — generating insights that nobody acts on.

- API-first integration with underwriting workbenches. The risk score or concentration flag generated by an analytics model must be surfaced at the point of underwriting decision — in the workbench, alongside the submission data, before the quote is issued. API-first architecture enables this: the analytics model is called at intake, returns a score within milliseconds, and the workbench displays it alongside other risk data.

- Embedded alerting in catastrophe monitoring dashboards. Early-warning analytics for concentration risk should feed directly into the catastrophe event monitoring workflow. When a weather event develops, the system should automatically calculate portfolio exposure in the event footprint and surface it to the CAT team — not require a data analyst to run a manual query.

- Automated pricing model triggers. For pricing teams managing large volumes of renewal business, real-time signals should trigger model re-runs when inputs change materially — not require manual scheduling. A telematics-driven score change, a large loss event in a geographic segment, or a significant shift in a claims trend KPI should all be capable of triggering an automated model update.

- Data governance integration. Every signal feeding the real-time pricing environment must carry lineage metadata: where it came from, when it was updated, and what quality checks it passed. Without this, the pricing model operates on data that may be stale or inconsistent — and the actuarial team cannot confidently attest to the data quality underlying the rate filing.

- Feedback loops from claims into pricing. The most valuable integration pattern is the closed loop: claims signals feed back into the pricing model on a defined cycle. Emerging claim trends detected in FNOL data or adjuster notes should update the risk scoring model within weeks, not quarters.

6. Challenges and Limitations of Real-Time and Early-Detection Analytics

A candid view of the challenges is as important as the business case. Pricing and risk leaders who understand the limitations design better programmes and manage stakeholder expectations more effectively.

Data Quality at Speed

The fundamental constraint of real-time analytics is that data quality problems are amplified, not resolved, by speed. A telematics feed with GPS drift errors produces inaccurate risk scores faster. A claims extract with inconsistent cause-of-loss coding produces misleading trend signals in real time. The investment in data governance and quality monitoring must precede — not follow — the investment in real-time analytics infrastructure.

Model Explainability and Regulatory Compliance

In insurance, pricing model explainability is a regulatory requirement, not a preference. The EU AI Act and GDPR classify many insurance analytics functions as high risk, mandating explainability assessments, dataset documentation, and post-deployment monitoring [Mordor Intelligence, 2026]. 58% of insurance companies have already implemented formal review processes for analytics models to ensure fairness and regulatory compliance — those that have done so experience 75% fewer regulatory challenges [KPMG, 2024]. In US states with strict rate filing requirements, the ability to explain a machine learning score component to a regulator is non-negotiable.

Data Latency vs. Stability Trade-Off

Not all pricing decisions benefit from the fastest possible data. A pricing model that updates continuously on telematics signals may introduce instability in the renewal process — policyholders receiving materially different renewal quotes than their mid-term pricing. The appropriate update frequency depends on the decision being made: real-time for individual risk scoring at quote, monthly or quarterly for portfolio-level rate adjustments, annually for the regulatory rate filing.

Legacy System Integration Complexity

Most carriers still manage core policy administration, billing, and rating through legacy platforms that were not designed for real-time data feeds. Connecting a streaming analytics environment to a batch-update policy administration system requires careful interface design, often including event-driven middleware layers. The integration cost and complexity is a significant underestimated item in real-time analytics programme budgets.

Talent and Capability Gaps

The demand for data engineers with cloud platform, streaming, and governance skills significantly exceeds supply across the industry. The Bureau of Labor Statistics projects 36% growth in demand for data scientists in insurance through 2026, significantly outpacing average job growth [Decerto, 2025]. Carriers building real-time analytics capabilities often find that the talent constraint is the binding constraint — not the technology.

Perceptive’s POV — On Managing the Limitations

The limitations of real-time analytics are real. But at Perceptive Analytics, we consistently find that carriers who use these limitations as reasons not to start are making a different kind of mistake. The data quality problem is solvable with the right governance investment — and that investment pays dividends across all analytics, not just real-time pricing. The explainability problem is manageable when the model architecture is designed for it from the start. The talent problem is addressable through the right vendor and partner strategy.

The carriers that make the most progress are those that accept that real-time analytics is a capability they will build over 12–24 months, not a platform they will install. They start with one high-value use case — telematics scoring for UBI, or a concentration risk dashboard for a specific peril — validate it, demonstrate ROI, and extend from there. The approach is incremental. The ambition is not.

7. Business Case and ROI: Cost-Benefit of Real-Time and Risk Analytics

The ROI of real-time analytics in insurance pricing is not a single number — it is a portfolio of benefits across pricing adequacy, adverse selection, operational efficiency, and capital efficiency. Each benefit carries a different time horizon and measurement approach.

Pricing Adequacy and Premium Leakage Recovery

Premium leakage — the gap between charged and technically adequate premium across the portfolio — is the most direct benefit of improved pricing analytics. Willis Towers Watson’s 2024 research found that carriers implementing predictive modelling reduced leakage by approximately $14 million per $1 billion of written premium [WTW, 2024]. For a mid-market carrier writing $2 billion in premium, this represents a $28 million annual improvement in pricing adequacy — achievable without top-line premium growth.

Loss Ratio Improvement

74% of insurers implementing real-time risk assessment tools have reduced loss ratios by 3–5% [Mordor Intelligence, 2026]. On a combined ratio of 96–98%, a 3–5 point loss ratio improvement is the difference between meaningful underwriting profit and breakeven. The P&C industry’s combined ratio improved by 500 basis points from 2023 to 96.6% in 2024 [IRMI, 2025] — real-time analytics is one of the structural drivers of that improvement.

Adverse Selection Reduction

Adverse selection — the systematic tendency to attract higher-risk insureds when pricing is inadequate for a segment — is difficult to measure directly but highly measurable in its consequences: loss ratio deterioration in specific segments, higher-than-expected large loss frequency, and renewal retention rates that skew toward the worst-performing accounts. ML-driven pricing models that detect and correct adverse selection exposure before it accumulates in the portfolio produce capital-efficient underwriting results that simple portfolio rate increases cannot replicate.

Concentration Risk Capital Efficiency

Carriers that can identify and manage concentration risk in real time — rather than discovering it post-event — require less catastrophe reinsurance to achieve the same capital adequacy outcome. The ability to understand and actively manage PML against a real-time event footprint has direct reinsurance cost implications. For carriers writing in catastrophe-exposed geographies, this is often the largest single ROI component of a portfolio analytics investment.

Implementation Investment Ranges

Total investment for a real-time analytics programme varies significantly with scope. A focused initial build — telematics scoring for personal auto, or a concentration risk dashboard for a single peril — typically requires 6–12 months and investment in the range of $500,000 to $2 million for infrastructure, data engineering, and modelling talent. Enterprise-scale programmes with multiple lines of business, streaming ingestion, and integrated early-warning systems range from $3 million to $8 million over 18–24 months. Many insurers report ROI within 12–24 months of rollout when the initial use case is correctly scoped [RTS Labs, 2025].

| ROI Driver | Mechanism | Typical Benefit Range |

|---|---|---|

| Premium leakage recovery | More accurate individual risk pricing reduces underpricing | $12–15M per $1B written premium |

| Loss ratio improvement | Better risk selection, real-time signal integration | 3–5 percentage points |

| Adverse selection reduction | ML-driven segmentation identifies repricing before deterioration | Measured in renewal loss ratio delta |

| Reinsurance cost efficiency | Real-time concentration monitoring reduces PML uncertainty | 5–15% reduction in CAT reinsurance premium |

| Operational efficiency | Automation of pricing reviews and data preparation | 30–50% reduction in analyst time |

8. Case Examples of Successful Real-Time Pricing and Early Risk Detection

Case Snapshot: Personal Auto — Telematics-Driven Pricing and Loss Ratio Improvement

A personal lines carrier writing standard and non-standard auto implemented a mobile telematics programme integrated directly with its rating engine. Individual driver risk scores — generated from speed patterns, braking frequency, and time-of-day driving — were translated into pricing adjustments at renewal. Within 18 months, the carrier achieved a 27% improvement in loss ratios for the telematics-enrolled segment through granular risk segmentation, while telematics-enrolled policyholders exhibited significantly lower retention risk: 82% of enrolled policyholders reported they would recommend the programme to other drivers. The key integration decision — connecting the telematics scoring API directly to the renewal rating engine, rather than running it as a separate analytical exercise — was the difference between a pricing capability and a pricing decision tool.

Case Snapshot: Commercial Property — Geospatial Concentration Risk Dashboard

A mid-market commercial property carrier with significant exposure in hurricane-prone coastal markets implemented a geospatial analytics platform that geocoded 100% of its commercial property portfolio and overlaid parcel-level exposure data against a real-time CAT event monitoring feed. When Hurricanes Helene and Milton developed in Q4 2024, the carrier was able to calculate its exposure within the evolving event footprint in real time — before claims were filed — enabling proactive reserve setting and CAT team deployment. The platform identified a previously undetected accumulation of high-value commercial properties within a two-mile coastal band in a single county, triggering a portfolio review that adjusted aggregate limits in that geography. The reinsurance cost saving from the improved PML management exceeded the platform implementation cost in the first renewal cycle.

Case Snapshot: Casualty — Social Inflation Early Warning System

A specialty casualty carrier with significant general liability and umbrella exposure began integrating a verdict database and litigation filing rate feed by jurisdiction into its pricing monitoring workflow. The analytics identified three jurisdictions where nuclear verdict frequency was accelerating at twice the national rate — 12 to 18 months before the loss development would have been visible in standard actuarial triangles. The carrier made targeted rate adjustments in those jurisdictions ahead of the market, avoiding the combined ratio pressure that competitors experienced when the deterioration became apparent. The early-warning signal was detected not through actuarial reserving but through a real-time monitoring dashboard that tracked verdict data and attorney filing patterns as leading indicators.

Perceptive’s POV — On Case Study Patterns

The common thread in successful real-time analytics implementations is not the sophistication of the technology — it is the clarity of the decision it was designed to support. Each of the cases above started with a specific question: ‘What is our exposure in this event footprint before claims are filed?’ or ‘Where is social inflation accelerating before it shows up in our loss development?’ The analytics was built to answer that question, connected to the workflow where that answer would be acted on, and measured against the outcome it was designed to improve.

At Perceptive Analytics, we consistently find that carriers who start with a specific decision — and build backwards to the data and model needed to support it — achieve better and faster ROI than those who build a platform first and look for use cases afterwards.

9. Practical Next Steps for Pricing and Risk Teams

For pricing and risk leaders evaluating real-time analytics investment, the following sequence consistently produces better outcomes than large-scale platform builds that attempt to solve everything simultaneously.

Step 1 — Conduct a Signal Audit (4–6 Weeks)

Before selecting technology, assess what real-time signals you already have access to — or could access with manageable integration effort — versus what you are using today. Most carriers have telematics data they are not fully exploiting, claims signals they are not systematically monitoring, and geospatial exposure data that is not integrated with their PML models. The signal audit identifies the highest-value, lowest-cost starting points.

Step 2 — Define the Decision You Are Automating or Accelerating (2–4 Weeks)

Every real-time analytics investment should be traceable to a specific decision: the renewal pricing decision on telematics-enrolled auto policies, the aggregate limit decision in a cat-exposed geography, the rate adjustment in a jurisdiction showing social inflation acceleration. If the analytics cannot be connected to a specific decision and a measurable outcome, the investment case will not survive scrutiny — and should not.

Step 3 — Pilot on One Use Case Before Scaling (3–6 Months)

Choose one high-value, bounded use case — personal auto telematics pricing, or concentration risk monitoring for a single peril — and build end-to-end: data ingestion, model, decision API, and dashboard. Run it in parallel with the existing process. Measure the pricing adequacy or loss ratio outcome against the baseline. The pilot produces the ROI evidence that justifies the enterprise programme and the operational experience that prevents expensive mistakes in the scale phase.

Step 4 — Establish Data Governance Before Scaling (Ongoing)

As the analytics environment grows, data governance must grow with it. Every new data source requires ownership, quality monitoring, lineage documentation, and access controls. Actuarial attestation of data quality is a regulatory requirement in most jurisdictions. Building governance as an infrastructure layer from the start — rather than retrofitting it when the regulator asks — is the difference between a sustainable analytics programme and one that creates compliance risk as it scales.

Step 5 — Prioritise Talent and Operating Model Alongside Technology

The technology is the easier part. The harder work is building the operating model: who owns the pricing model, who monitors the concentration risk dashboard, who is accountable for data quality when a signal goes stale. Carriers that achieve the most from real-time analytics have defined roles — a dedicated model owner, an embedded analytics team in the pricing function, and executive accountability for data quality — not just a technology platform.

The window for competitive advantage through real-time pricing and risk analytics is real, but it is closing. 88% of auto, 70% of home, and 58% of life carriers are already moving toward AI-enabled operations [Mordor Intelligence, 2026]. The question for pricing and risk leaders is not whether to build this capability — it is how to build it in the right sequence, with the right governance, and connected to the decisions that actually move the loss ratio.

Perceptive Analytics — Closing Perspective

Real-time analytics does not replace actuarial judgment. It gives that judgment better information, faster. The actuary who can see a social inflation trend 12 months before it shows in the triangle makes better pricing decisions than one who sees it in the reserve review. The underwriting leader who can calculate concentration risk in a developing CAT event footprint manages capital more effectively than one who waits for the claims run.

At Perceptive Analytics, our work with pricing and risk leaders starts with the decision — the specific underwriting or risk management outcome that better information would improve — and works backwards to the data architecture, the model, and the integration pattern that delivers it. If you would like to understand which real-time pricing or concentration risk use case would deliver the highest ROI for your portfolio — and what it would take to build it — that is exactly the assessment Perceptive Analytics is equipped to provide.

Quick Diagnostic: 10 Questions for Pricing and Risk Leaders

| 1 | What is the lag between a material risk event and your pricing model reflecting it? |

| 2 | Can you calculate your portfolio’s exposure in a developing CAT event footprint before claims are filed? |

| 3 | Do you have a real-time view of where social inflation is accelerating in your casualty book, by jurisdiction? |

| 4 | What percentage of your underwriting decisions are informed by ML-driven risk scores versus GLM factors alone? |

| 5 | How quickly can your pricing team detect a segment-level shift in loss ratio — weeks, months, or at quarter-end? |

| 6 | Do you monitor counterparty or contractor concentration in your commercial property book? |

| 7 | Is your telematics or IoT data connected to your rating engine, or is it used only in retrospective analysis? |

| 8 | Who owns data quality for the external signals feeding your pricing models? |

| 9 | How many sources of data does your pricing team access manually when building a rate review? |

| 10 | If a new peril emerged — a novel chemical liability, a new weather pattern — how quickly could your models incorporate it? |

Sources & References

[1] Munich Re (2024). Natural Catastrophe Statistics. https://www.munichre.com/en/risks/natural-disasters.html

[2] IoT Insurance Observatory / Carrier Management (February 2026). https://www.carriermanagement.com/features/2026/02/11/284454.htm

[3] GM Insights (2025). Insurance Telematics Market. https://www.gminsights.com/industry-analysis/insurance-telematics-market

[4] IMARC Group (2024). IoT Insurance Market. https://www.imarcgroup.com/iot-insurance-market

[5] Verisk (2025). 2025 Annual Insurance Claims Trends Report.

[6] n2uitive / Industry Research (2025). https://n2uitive.com/blog/insurance-claims-statistics-trends

[7] Aon (2025). https://www.aon.com/en/insights/articles/5-top-trends-risk-capital-2025

[8] Capgemini (2024). World P&C Insurance Report 2024.

[9] Goldman Sachs / RTS Labs (2024). https://rtslabs.com/predictive-analytics-in-insurance/

[10] WTW (2024). Predictive Modelling in Underwriting.

[11] Mordor Intelligence (2026). Insurance Analytics Market.

[12] Allstate / Softwebsolutions (2025). https://www.softwebsolutions.com/resources/data-analytics-in-insurance/

[13] Accenture (2024). Insurance Technology Vision.

[14] IRMI (2025). 2024 Insurance Year in Review. https://www.irmi.com/articles/expert-commentary/2024-insurance-year-in-review-and-2025-developments

[15] KPMG (2024). Compliance survey.

[16] Gartner (July 2025). Market Trend: Cloud Shift in Insurance.

[17] RTS Labs (2025). https://rtslabs.com/predictive-analytics-in-insurance/

[18] Decerto (2025). https://www.decerto.com/post/insurance-software-with-predictive-analytics-a-competitive-edge

Ready to build real-time pricing and concentration risk capabilities for your portfolio?

Talk with our consultants today.